Calculating Cash on Cash Return from Multiple Properties

The gist of this exercise is to get data from Zillow, import it into excel using the “Zillow to Excel” Chrome extension, and then creating another custom tab on the Excel file to analyse the data. We take annual income minus expenses and divide that over our cash investment which consists of our downpayment and closing costs. If there is rehab or initial repair work that would also be in the denominator.

Watch for yourself and see if you can make your own cash return spreadsheet to find the best deal! If you wouldn’t mind I’ve love for you to subscribe to my YouTube channel while you’re at it by clicking on the video via the “Watch on Youtube” link and subscribing.

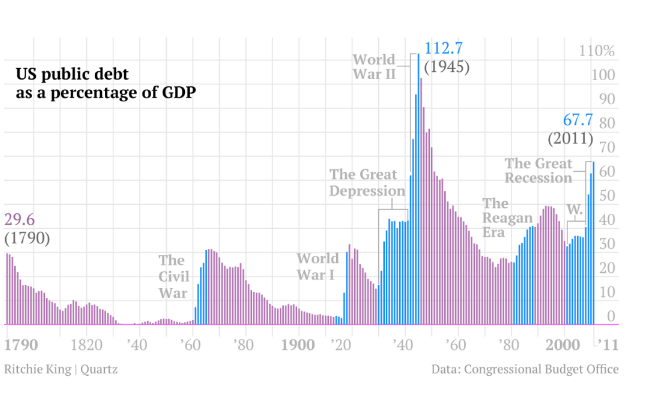

20 Years Since US Government Ran a Surplus

“The principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale” -Thomas Jefferson

“Government debt is a system, not only ruinous while it lasts, but one that must soon fail and leave us destitute” – Abraham Lincoln

If you’ve graduated from university in the past 20 years most likely you’ve been taught that deficit spending is good for an economy, you’re also most likely aware that for the past 20 years that we’ve had consistent government deficit spending. The last time the government ran a surplus was between 1998 to 2001. Going back further the last surplus before 1998 was in 1969 when Nixon took office. The period between including the 70’s and 80’s the US experienced high inflation but on paper PPP per capita GDP also went up. If you look at the chart below the Federal Debt was still less than 60% of GDP throughout the 70’s and 80’s but as of the latest data reported at the end of 2020 we are currently at 127% Debt/GDP.

Federal Debt as % of GDP

The last time the US has ever had this much Federal Debt was back in 1945, when the US had not only spend a lot of money on Roosevelt’s New Deal to get out of the Depression but also we had spent an enormous amount of money on bringing an end to WWII.

US Public Debt Historical

The US has disastrously mismanaged the COVD-19 crises and unfortunately had to pay a lot of money because of it. How many rounds of stimulus will be enough, or will this become the new normal? A major beneficiary of this stimulus has been the stock market and real estate has been buoyed by historically low interest rates. However I think our consumption economy may have rough seas ahead unless it can tackle a few issues:

- Tax Evasion by Mega-Corporations – Without getting too much into specifics large corporations have ways to avoid taxes, a luxury not available to smaller businesses. This is a double edged thorn because not only does it stifle competition but also it further contributes to a growing national debt. Add lobbyists to the equation and the little guy has his work cut out for him. Ironically for us the investor class it means we should “go with the flow” and make sure we are at least riding the wave of blue chips and the Silicon six to retirement.

- Boosting manufacturing – the US needs to produce goods especially high tech manufacturing so it does not become eclipsed by other countries. It needs to make sure it can make medicines and vaccines domestically as well as cutting edge semiconductors, batteries, and circuit printing. Even though Intel is I would say one generation behind other companies I think the US needs to focus on getting it and other manufacturers caught up with, for example, Taiwan and South Korea.

- Repair infrastructure that was built in the 60’s. A lot of the US, especially the power grid and train systems, are woefully out of date. Rather than just giving money away, expanding the idea of UBI, the US should emphasize infrastructure from roads, electricity, trains, hydroelectric, and nuclear energy. Solar panel construction should only be done after evaluating the carbon cost of production and disposal, as well as impact on local environments.

- The Suburbs. The Suburbs as a concept were well-intentioned, but common sense and other towns across the world show that it really makes more sense for people to live closer if not walking distance from where they work. Strictly regulated commercial vs residential zoning should be re-evaluated so that people don’t need to travel by car or by train for that matter for everyday life. I think this will become essential as populations grow and in the US as the dollar starts to lose its status as the reserve currency.

So in conclusion, the US has some time left to fix a few things before the Federal Debt becomes an issue too hard to handle. It needs to use the time it has leverage as the world’s reserve currency to put the value of the currency to good use to put us on solid ground going into the future. Other countries have been keeping our standard of living up by creating cheap goods and accepting US dollars for them even though they know we can create dollars out of thin air. The Federal Reserve should keep it’s interest rates low while this transition takes place so the Government Debt doesn’t spiral up to 200% of GDP. Banks should be vigilant as they dole out mortgages with low interest rates to avoid another massive real estate bubble.

Is this going to happen? Probably not. Another large scale event like Covid, such as a new war would really cause issues with our government debt and most likely also crash the stock market. Stagflation may be the new buzzword and everyone will be wishing they were holding gold or bitcoin instead of stocks.

What’s the Future of Bitcoin?

What’s Happened in a Year

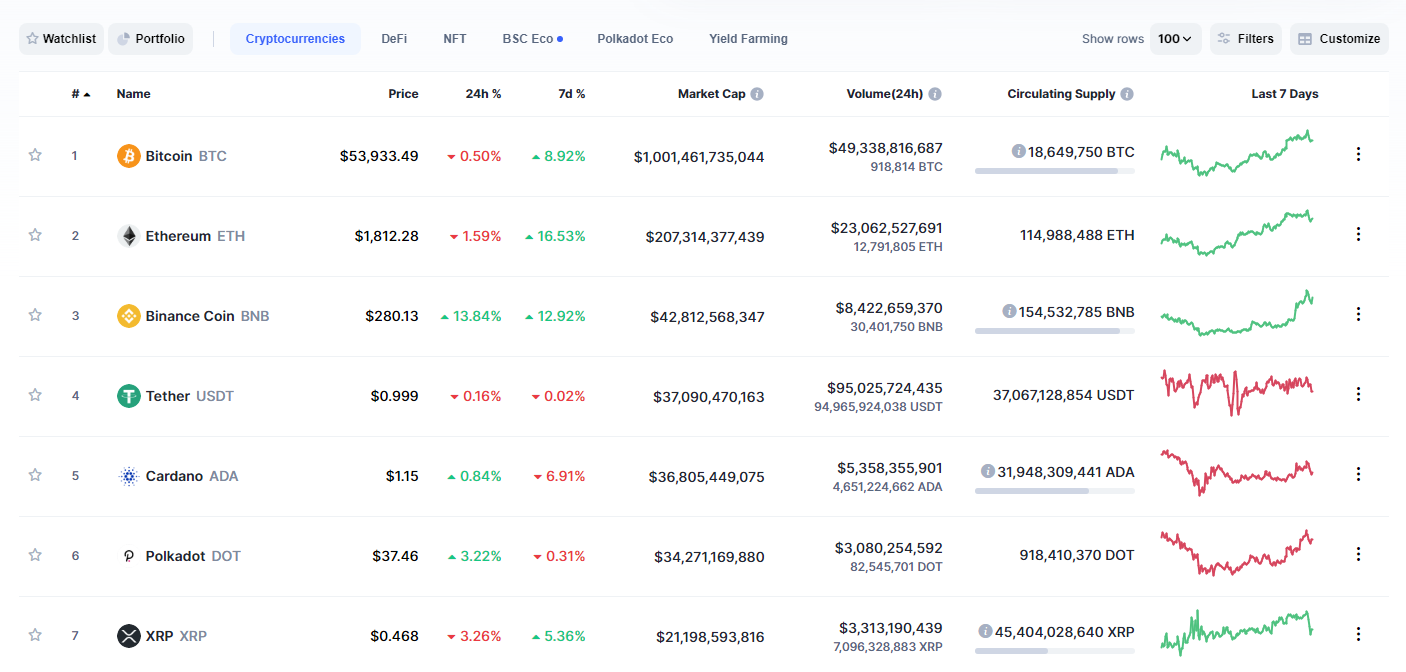

So unless you’ve been sleeping under a rock without wifi you’re probably aware that bitcoin has made an astounding jump from about $8,000 to $54,000 in a year. A single bitcoin can now be a downpayment for a house, 31 ounces of gold (today’s gold spot price is $1,710), and depending on where you live in the world a year or two of retirement in comfort.

Now what’s the future of bitcoin? Should I keep it or sell it? Is it going to be killed off by quantum computers?

Should I keep or sell bitcoin?

I wouldn’t sell all my bitcoin just because the price has gone above $50,000. If you would like to use the money in other investments such as real estate I think it would be prudent to sell enough to buy a house but don’t sell everything because I think you’ll regret it. If you’ve made money on bitcoin via Robinhood I suggest getting rid of it and converting it to “real” bitcoin on your controlled wallet as soon as your situation allows. Keep in mind taxes while you do this.

The whole point of the rise of bitcoin is getting away from holding cash, and putting money in bitcoin puts you in a limited supply cryptocurrency recognized and accepted in many places around the world as a store of value. Not unlike gold has been, which I will get to later.

Should I buy more bitcoin?

Keep in mind bitcoin historically has had huge pumps and then dumps, falling in 2017 from 20k down to the low 3k’s. Maybe this time is different, maybe not. Yes there are a lot more institutions buying up bitcoin such as Tesla and major banks and investment firms, but the possibility still exists for bitcoin to fall and hurt people that put money they depended on in this. If you still want to buy at current prices (mid 50k’s) I’d dollar cost average over a longer period of time by setting aside a few hundred dollars per month to purchase. I’m bullish myself on the long term prospects, but can see the coin drop all the way back to 20k and if that does happen it will be a great time to pick up more.

To me, bitcoin is like gold in a few other aspects. Gold has been around since early civilization, it may not be the smartest thing to carry around to do day to day transactions with but has been recognized a good store of value that is not easily defiled. Other cryptocurrencies that have come out since are not as distributed as bitcoin, meaning they are more easily taken over and manipulated and or controlled by a central authority. Yet even other cryptocurrencies are not “mined” but instead “pre-mined” and distributed by a central node (such as Algorand). However, these other coins have features such as “proof of stake” which allow in their algorithms to dole out “interest” to existing coinholders. Coins with this feature include but are not limited to: Algorand, Cardano ADA, Cosmos, and Tezos. Of these Cardano ADA has by far the highest market cap with 36.8B as of today (March 9th, 2021). That’s still dwarfed by bitcoin’s enormous 1.001 T market cap. At the bottom of this post you can explore some details on various cryptos but you’ll see that bitcoin is closest to reaching its max supply of 21 million coins. Once that hits we may see price rise even further.

Crypto Market Cap

Should We Worry about Quantum Computers?

Short answer, yes. Quantum computers are far from being mature enough to run sustainably and accurately enough to overload bitcoin mining processing power to overtake 50% computing power and delegitimize the transaction verification process and spoof transactions. However, as the technology improves (and it will) it will post a larger threat to bitcoin. That being said, bitcoin can be upgraded if enough of the miners choose to upgrade and it would be in their best interest to do so to start to build improvements as Quantum computer mature. The largest threat in my opinion would be a state actor working in secret building up Quantum Supremacy before bitcoin (and other encryption used throughout the world for that matter) can adapt itself. I wouldn’t worry about it in the next five years.

If this possibility scares you away from Crypto, I’d just settle for real estate and gold. Any assets not on or depending on the internet for that matter, because ultimately banks and financial institutions and the internet itself and all that rely on it could technically be broken with a mature Quantum computer. All encrypted information over the internet would be at risk.

The bottom line is a new form of cryptography needs to be put in place ASAP before Quantum Computers can be used to destroy the internet, I’m not super worried this doomsday event will occur because safeguards will be built beforehand.

Let’s Talk about Bitcoin Versus Gold

Bitcoin Versus Gold

The gist of this article is to explain in clear English why bitcoin has outperformed gold and makes a more viable currency. I’m not going to speculate on price movements rather the utility of the currency. If you’re an older reader pay closer attention, bitcoin is no longer just “an idea in a geek’s head”.

The Charts

BTC/USD 1 Year to Jan 9, 2021

SPRD Gold Trust Price 1 year history ending on Jan 9, 2021

Why has Bitcoin Outperformed?

So why has bitcoin outperformed gold in the past year? The charts above show bitcoin and a gold ETF side by side and as you can site bitcoin is the clear winner. My answer is in the form of a question.

“How would you use gold to buy what you buy in a given year?” How can you use gold to buy pizza, how can you use gold to order items online, and how can you use gold on the go anywhere you are?

The answers are clear, you can’t. If you do, you’ll probably lose value, for example you can give a store clerk a gold coin and he’ll pocket it and then pay from his pocket because he just ripped you off, but he won’t go through the rigamarole of checking the spot price of gold and empty out his cash register to make it a fair transaction. Regarding online orders, forget it. It’s really dangerous and stupid to be carrying gold coins with you everywhere you go.

Now pose the same question with bitcoin. Well, in some foreign countries such as Japan I can buy pizza with bitcoin. The US is still catching on so most restaurants and stores will not accept bitcoin. Many websites accept bitcoin, a long time WordPress started accepting bitcoin and others followed such as Steam, Reddit, Microsoft, AT&T. The biggest news of all I think is that Paypal will allow spending in local currencies with bitcoin. So you go anywhere in the world, imagine being able to spend in local currencies being converted out of bitcoin and a real-time rate. Amazing right? All you need is your phone, something undoubtedly you have either in your hand or pocket right now. Good luck bringing gold overseas, even locally TSA questions people that move gold around but if you go overseas you may be subject to paying a tariff to bring in gold.

What should I do if I have Gold?

If you have gold don’t worry, I think gold prices will keep going up in the medium and long term. A short term fall is most likely institutions rebalancing as they add bitcoin to their portfolio. Institutions need to have bitcoin in reserve if they offer their customers the option to buy bitcoin on their platform. Gold does have a few benefits over bitcoin, including it’s time earned reputation as a store of value. A digital coin that’s been around for a little more than 10 years is not going to replace gold as the “gold standard”, and you are protecting yourself against inflation. Gold also has the title of being anonymous. As long as people aren’t writing down serial numbers of coins or bars they trade, gold can be untraceable. Bitcoin used to have that distinction but since it uses a public ledger if folks reuse their same bitcoin addresses its possible to trace down where addresses belong using some tricky sleuthing. Also, many people are keeping bitcoin on online wallets that are hosted by companies rather than keeping it in cold storage on hard drives. That means users don’t really own the wallets they are using a service to manage a wallet that then creates sudo wallets when transactions are performed.

You’ll want to make precautions to make sure you don’t get your gold lost or stolen, gold thankfully has elemental properties that prevent it from decaying or becoming dull over time. That being said, I feel it’s value as a currency are less than bitcoin so treat it more as a hard asset investment (much like real estate except without the power to cash flow). I’m going to get to preferred investments later.

What should I do if I have Bitcoin?

If you have bitcoin congratulations, you’ve probably already made a killer profit. That being said bitcoin is still growing as a currency and most folks that are older and less technology savvy may be less likely to “catch on”. However, the great thing about bitcoin is it is a deflationary currency meaning it has a hard supply cap and the mining becomes more difficult over time. Higher demand with limited supply will lead to higher prices, however a pullback from the recent price spike is very possible. What I would do if I did not already own real estate is sell enough bitcoin to make sure you own your primary residence. If you have a lot of bitcoin I’d also sell more to buy rental properties which pay back the mortgage and then some. Throughout time mankind has had great success in making fortunes from supplying housing to folks for a price. You are doing tenants a service by providing housing at a price they are willing to pay and they do not have to buy an entire house or deal with some struggles that come with owning properties such as maintenance, taxes, insurance. I wouldn’t sell it all though because during a rising period it’s hard to be certain how high bitcoin will go. Will it stop at $50,000 or continue it’s way to $1,000,000? With a max supply of 21 million coins a 1 trillion dollar total capitalization would mean each coin is worth $47,619. Does the world place that much value on this cryptocurrency? My guess is yes, and if bitcoin pulls back to less than $20,000 I will be dollar cost average purchasing more with each paycheck.

The Paycheck Conversion Plan

I learned of this when I lived in Malaysia. The Malaysia ringgit was getting hit hard with low oil prices and political issues, lines would form around all the currency traders (which were prevalent also because of lots of tourism). Locals would exchange their hard earned ringgit for either USD (US Dollars), SGD (Singapore Dollars), or RMB (Chinese Money). The reason for this was to prevent their money losing value as fast as it would otherwise. Also because they trusted the other currencies more.

I think it’s a great painless and stress free way of purchasing something your brain construes as “expensive” over time. Kind of like getting into the ocean inch by inch rather than taking a dive. Budget yourself, how much you need for your life and how much you use for investing. Divide your investing into stocks,real estate, and crypto. Divide your crypto into Bitcoin, Etherium, Litecoin, and any other coins you deem worthy (read the white papers and do so checking on how easy these coins are to mine and what they are already used for). After you come up with that percentage multiply it by your wages (be it bi-weekly, monthly, etc) and then set a recurring purchase transaction on a website like Coinbase (join using this link to get $10 free bitcoin for you and me) for all the coins you’ve come up in your list.

I hope this has been helpful, please subscribe to our free mailing list.

https://www.facebook.com/TheHighestReturn

Biden Stocks

Which stocks will benefit from a Biden presidency?

Tonight’s first Presidential debate may have a lot of people thinking about their stock portfolio. Should I sell everything? Should I buy everything? Or is there a way I can position myself to be in better shape if the incumbent loses the White House. Like you, I have no idea who is going to win but have some ideas on what stocks will benefit from a Biden presidency based on the policy changes that would occur. Let’s take a look at some losers and then winners of a Biden presidency.

Losers

Let’s start with the stocks that will be at higher risk with a Biden presidency. Trump has always advocated de-regulation and privatization of public lands for profit. This largely benefits energy companies operating in the US in the fossil fuel industry. Extracting oil and natural gas would become less profitable under a Biden presidency, so you could consider investing AGAINST Exxon Mobil (NYSE:XOM), EOG Resources (NYSE:EOG), Marathon Oil (NYSE:MRO). Buying put option spreads with expiration a few months into a Biden presidency would make sense.

Strategy

I would not naked short a dividend paying stocks because it means you have to pay the dividends to who you short the shares from, through your broker. Buying a put spread means you benefit from a declining price, but limit the price you pay to buy the put option since you are also selling a put option at a lower strike price.

Winners

Now lets take a look at some companies that will probably benefit from Biden. Biden’s policy website has it’s own page for clean energy plans, and it specifically emphasizes solar and wind technologies. I am a big fan of Vestas (OTC:VWDRY), a Danish company with operations in the United States holding the title as largest wind company in the world. I own shares of this company and it’s my preferred “green energy” stock. Another benefit of Vestas over another company involved in wind such as General Electric (NYSE: GE) is that it’s not as diversified. GE is in the business of fossil fuel power plants and a variety of different sectors which will diminish the gains experienced by green energy by the company. For that reason I do not favor buying GE at this juncture.

Tesla (NASDAQ: TSLA) will benefit from a push to move from gas/diesel automobiles to EV’s, as states like California push for EV mandates for personal and commercial vehicles. A Democratic presidency or series or presidencies would give the EPA more power to regulate and push consumers towards electric vehicles. Gasoline prices would be higher all things being equal with higher regulations on drilling and the business of oil and gas industries. Chinese competitor Nio (NYSE: NIO) will most likely rise alongside Tesla.

I own both Tesla shares and NIO shares.

Strategy

I hold VWDRY, TSLA, and NIO as long positions. Option strategies include buying call option spreads for these stocks with expiration after the election, or selling PUT options for a stike price near the money after the election.

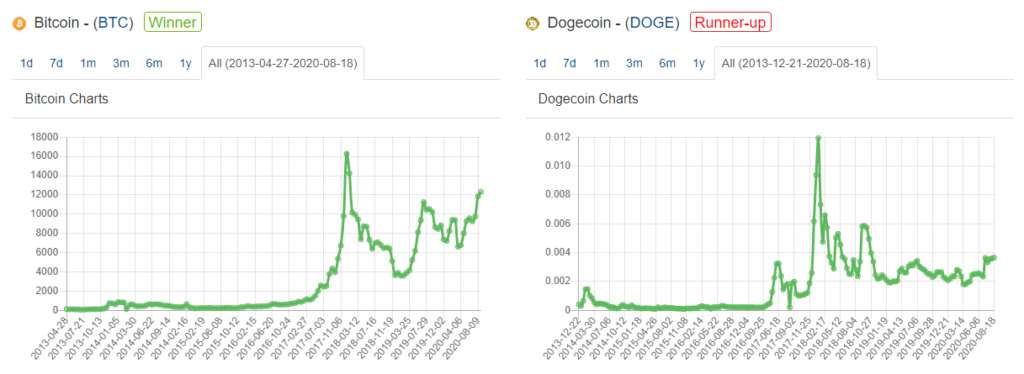

Why Bitcoin Trumps Dogecoin

Ok Dogecoin is cheap. Very cheap. Today it’s trading at $0.00351056, which makes it appealing the penny stock traders and the like who want to make it to the moon. I personally hold 50,000 of these coins, but do not believe in them. Here’s why:

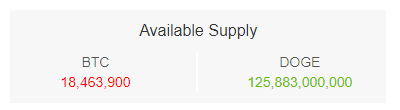

- The supply of Bitcoin is constrained. The algorithm only allows for 21 million to ever be mined. That makes it harder to flood the market and drive prices down through the floor.

- The supply of dogecoin is 8 turned sideways. That makes this an inflationary currency and no better than the USD.

Additional Information

- Bitcoin is the gold standard of crypto, and built off the idea that currency can be democratized and protected against central bank shenanigans, Dogecoin was founded off a meme of a dog.

- Alternatives to Bitcoin that have a supply cap are:

- Etherium

- Litecoin

- Ripple (I have qualms with Ripple since a lot of the supply has been pre-mined and gets released periodically, sounds like manipulation to me)

US Debt 25 Trillion and Counting. How to Protect Yourself.

The United States is 25 trillion dollars in debt. It collects around 3.2 trillion dollars in tax revenue every year and spends 6.2 trillion dollars every year. The spending continues to go up and all the while the US is paying interest on its debt. Instead of hoarding dollars you should consider some of these other stores of value.

The US dollar is one of the strongest currencies out there, backed by the strongest military and economy the world has ever seen. That being said it is not in the interest of the United States government to have the US dollar increase in value, especially because it owes so much in the form of Treasury bonds and notes. Thankfully most debt is internal – meaning the debt is held by US entities and the Federal Reserve, however there is a lot of debt owned by foreign countries as well. This makes inflation FAVORABLE for multiple reasons – the amount owed to others decreases in real value and economic growth occurs when people use their money to make a higher return than inflation and the interest rates.

If the Federal Reserve were to increase interest rates it would strengthen the US dollar, going against the interests I mentioned above.

This is fine, you just need to know where to put your money so you aren’t affected as much by it.

Watch and subscribe.

Adam Interviews Damien

Watch the interview between Adam and Damien, and how a index fund investor is starting to doubt what he believed strongly all these years. We go over when we started investing, what tools we use, and how we determine what to put our hard earned money into.

The takeaways are as follows:

- Damien invests into an index fund and about 10% into bonds.

- Adam believes index funds include winners and losers, and attempts to pick the winners directly. He also points to unethical companies being in the mix when you buy the whole market.

- Damien manages a budget sofware YNAB and Adam just uses his credit card to track spending. Both agree restaurants and eating out are a cash drain.

- Adam contends that if you have a 401k you’re already forced into buying stocks you can’t pick so why do that in your managed portfolio?

- Adam talks about bitcoin and gold being good alternatives to cash rather than just stocks.

- Damien insults Adam’s hair

- Adam insults Damien’s yearly return on investment (ROI)